Oliver Blume: "La reestructuración del Grupo Volkswagen llevada a cabo durante los últimos tres años está dando sus frutos".

«La reestructuración del Grupo Volkswagen llevada a cabo durante los últimos tres años está dando sus frutos. En todo el grupo. Para el conjunto del año, esperamos unos resultados sólidos, por encima de los del año anterior, en un entorno difícil, a pesar de que nuestro resultado operativo en el primer semestre se situó en torno a un 12 % por debajo del del año anterior. A nivel mundial, hemos entregado más coches que el año anterior, excluyendo el mercado chino, que sufrió una caída del 20 %. Nuestra cartera de pedidos también refleja una tendencia positiva: más de 70.000 pedidos de nuestra nueva familia de coches eléctricos urbanos en torno al ID. Polo en tan solo unas semanas, y los pedidos de vehículos totalmente eléctricos en Europa aumentaron más del 50 % en el segundo trimestre. Nuestros productos están obteniendo las mejores puntuaciones en pruebas comparativas, premios y estudios de calidad. Gracias a una gestión disciplinada de los costes, hemos logrado compensar los continuos y inevitables contratiempos, que se cifran en miles de millones de dos dígitos. Al mismo tiempo, el entorno para la industria del automóvil sigue siendo extremadamente difícil: crisis geopolíticas, conflictos comerciales, elevados requisitos normativos, mercados volátiles y una competencia cada vez más intensa. En un escenario de riesgo sin precedentes, el Grupo Volkswagen entra en la siguiente fase de su transformación, desde una posición de fortaleza y con una visión clara de las oportunidades que se avecinan. Con el programa más completo y de mayor alcance de la historia de la empresa, que abarca productos, tecnologías, competitividad, estructuras y áreas de crecimiento. Con nuestro plan de futuro, seremos aún más innovadores, más rápidos, más atractivos y más sólidos, y garantizaremos de forma sostenible el éxito del Grupo Volkswagen».

Oliver Blume, CEO del Grupo Volkswagen

“Estamos lanzando nuevos y atractivos vehículos, aplicando de forma sistemática nuestra estrategia de software y reduciendo las inversiones y los gastos generales. Al mismo tiempo, hemos generado un cash flow neto de 3.2 mil millones de euros en el primer semestre del año. A pesar de estos avances, nuestro margen operativo del 3,8 % sigue siendo demasiado bajo y pone de relieve la necesidad de actuar. En un entorno en el que el mercado chino total ha descendido un 20 % y los competidores chinos están aumentando sus exportaciones —y, con ello, la presión competitiva en Europa—, las iniciativas previstas actualmente no son suficientes.

Debemos acelerar los esfuerzos para reducir estructuralmente nuestra base de costes y mejorar de forma sostenible la calidad de nuestros resultados. Esto incluye mejorar las estructuras de costes de los vehículos, reducir los gastos generales, aumentar la eficiencia en nuestras plantas, acelerar el desarrollo tecnológico y agilizar los procesos de toma de decisiones.

Por lo tanto, debemos reducir significativamente la complejidad: en nuestra cartera de productos y plataformas, en nuestra cartera de participaciones, así como en nuestras estructuras de liderazgo y de toma de decisiones.

Lo que importa ahora es una implementación rápida y coherente”.

Arno Antlitz, CFO y COO del Grupo Volkswagen

Cifras clave

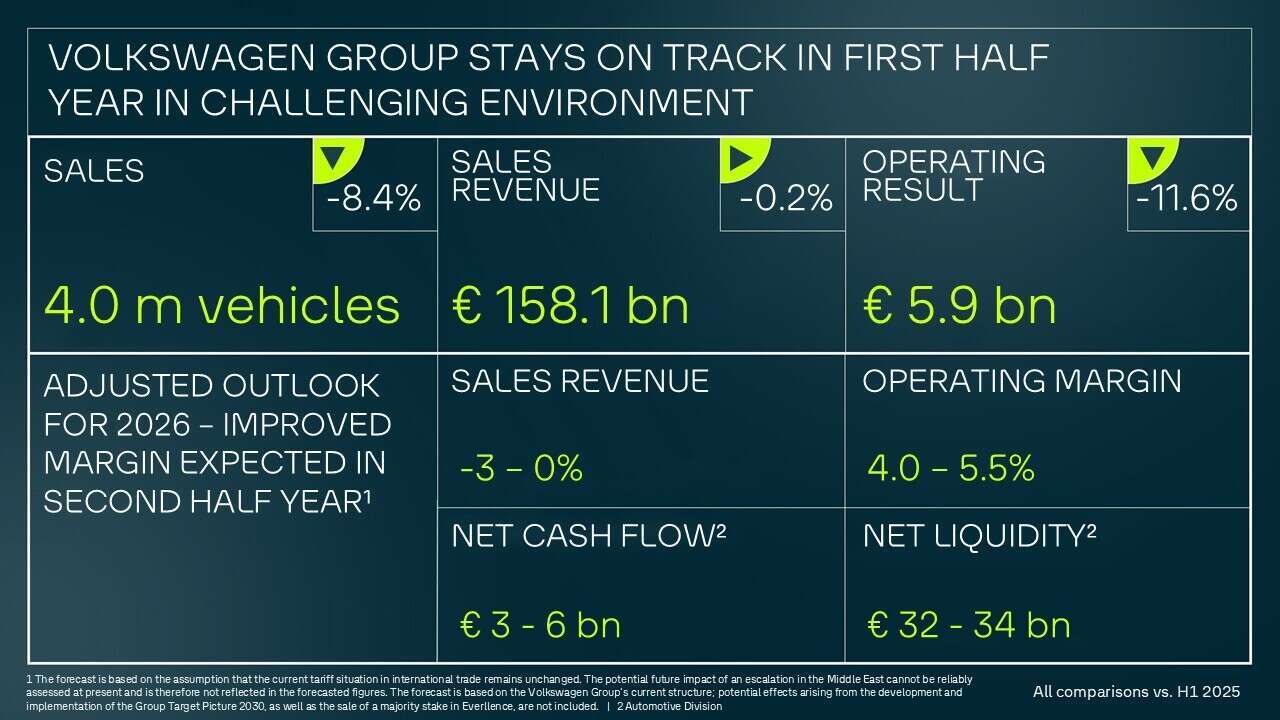

158.100 millones de euros en ingresos por ventas en el primer semestre de 2026, al mismo nivel que el año anterior (primer semestre de 2025: 158.400 millones de euros)

Los ingresos por ventas del primer semestre de 2026 se mantuvieron, en gran medida, al nivel del año anterior, a pesar de un entorno de mercado difícil (-0,2 %).

El aumento de los ingresos por ventas en el sector de los servicios financieros (+7,9 %) compensa casi por completo el descenso registrado en la división de automoción (-2,1 %). En el segundo trimestre, los ingresos por ventas ascendieron a 82.400 millones de euros (+2,0 %).

Resultado operativo de 5.900 millones de euros en el primer semestre de 2026, un 11,6 % por debajo del primer semestre de 2025 (6.7 mil millones de euros); margen operativo del 3,8 %

El resultado operativo se redujo en 0,8 mil millones de euros, debido principalmente a unos gastos de alrededor de 0,5 mil millones de euros relacionados con el cese de la producción del ID.4 en EE. UU., así como a efectos negativos de la composición de las ventas. La reducción de los costes derivados de las medidas de reestructuración, los efectos del tipo de cambio y la disminución de los costes fijos solo pudieron compensar parcialmente estos impactos negativos. En el segundo trimestre, el resultado operativo se situó en 3.5 mil millones de euros (-9,5 %), con un margen operativo sobre las ventas del 4,2 %.

6.900 millones de euros de resultado operativo antes de partidas extraordinarias en el primer semestre de 2026

Tras ajustar las partidas extraordinarias, como la paralización de la producción del ID.4 en Norteamérica y los costes de reestructuración, el margen operativo sobre las ventas en el primer semestre de 2026 se sitúa en el 4,3 %.

3.200 millones de euros de cash flow neto en la División de Automoción durante el primer semestre de 2026 (primer semestre de 2025: -1.400 millones de euros)

El aumento del cash flow bruto de 1.300 millones de euros, impulsado, entre otras cosas, por una menor carga fiscal, una reducción de las salidas de efectivo destinadas al capital circulante y un descenso de los gastos en inversiones en activos fijos e investigación y desarrollo, se tradujo en un sólido cash flow neto, significativamente superior al del año anterior.

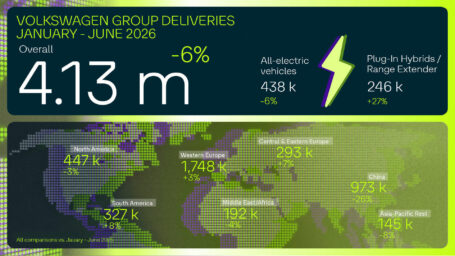

4 millones de vehículos vendidos en el primer semestre de 2026, un 8,4 % menos que en el primer semestre de 2025 (4,4 millones de vehículos)

El crecimiento registrado en Sudamérica (+5,2 %), Europa Occidental (+1,3 %) y Europa Central y Oriental (+9,6 %) solo compensó parcialmente las importantes caídas del mercado global en China (-31,6 %); Norteamérica registró un resultado ligeramente positivo durante el primer semestre del año (+0,9 %), tras el crecimiento registrado en el segundo trimestre.

La cartera de pedidos en Europa ha aumentado en torno a un 12 % en comparación con el cierre del ejercicio de 2025

La cartera de pedidos de vehículos eléctricos de batería (BEV) aumentó en más del 50 % en comparación con finales de 2025, y la cuota de los BEV en dicha cartera ascendió a más del 30 %. Con más de 70.000 pedidos, la gama de coches eléctricos urbanos está superando con creces las expectativas.

Previsiones para 2026

El Grupo Volkswagen prevé que los ingresos por ventas en 2026 se sitúen en un rango de entre el –3 % y el 0 % en comparación con el año anterior (anteriormente: rango de entre el 0 % y el +3 %). Se sigue esperando que el margen operativo del Grupo se sitúe entre el 4,0 % y el 5,5 %.

En la División de Automoción, la empresa sigue previendo un ratio de inversión de entre el 11 % y el 12 % en 2026. Se espera que el cash flow neto para el año 2026 oscile entre 3.000 y 6.000 millones de euros. Se prevé que la liquidez neta de la División de Automoción oscile entre 32.000 y 34.000 millones de euros en 2026. El Grupo Volkswagen sigue persiguiendo su objetivo de mantener una política sólida de financiación y liquidez.

Se prevén retos, en particular, derivados del entorno macroeconómico, las incertidumbres relativas a las restricciones al comercio internacional y las tensiones geopolíticas, el aumento de la intensidad de la competencia, la volatilidad de los mercados de materias primas, energía y divisas, así como los cambios en los requisitos derivados de la normativa sobre emisiones.

La previsión se basa en la hipótesis de que la situación arancelaria actual en el comercio internacional se mantenga sin cambios. El posible impacto futuro de una escalada de la tensión en Oriente Medio no puede evaluarse de forma fiable en este momento y, por lo tanto, no se refleja en las cifras previstas. La previsión se basa en la estructura actual del Grupo Volkswagen; no se incluyen los posibles efectos derivados del desarrollo y la implementación del «Group Target Picture 2030», ni la venta de una participación mayoritaria en Everllence.

Más información sobre los grupos de marcas

Core

El resultado operativo del primer semestre de 2026 mejoró significativamente hasta alcanzar los 3.600 millones de euros, lo que supone un aumento del 4,5 % con respecto al mismo periodo del año anterior. Los efectos positivos derivados de la optimización de los costes de los productos, la estricta gestión de los costes y las sinergias dentro del grupo de marcas se reflejan en una ligera mejora del margen operativo y en un aumento de los ingresos, a pesar de un entorno de mercado difícil y de una presión competitiva cada vez mayor.

El resultado operativo ascendió a 1.100 millones de euros, superando ligeramente la cifra del año anterior. En un entorno de mercado que sigue siendo difícil, factores como la estricta disciplina en materia de costes tuvieron un impacto positivo. El margen operativo se situó en el 3,8 % (año anterior: 3,3 %).

Automotive alcanzó un resultado operativo de 1.200 millones de euros (año anterior: 800 millones de euros). El margen sobre ventas fue del 8,0 %. Los ingresos ascendieron a 15.200 millones de euros (año anterior: 16.100 millones de euros). El cash flow neto de la división Automotive fue de 1.000 millones de euros, con un margen de cash flow neto del 6,7 %. Estos resultados se debieron a la reestructuración integral llevada a cabo el año pasado, a la sólida calidad de los precios y de la gama de productos, y a la reducción de los gastos relacionados con las provisiones a partir de 2025.

La cartera de pedidos de TRATON GROUP aumentó un 30 %, hasta alcanzar los 181.900 vehículos, en el primer semestre de 2026; con 21.100 millones de euros, los ingresos del Grupo se mantuvieron prácticamente al mismo nivel que el año anterior, mientras que el resultado operativo se situó en 942 millones de euros (-24 %) y el margen operativo fue del 4,5 % (-1,4 puntos porcentuales).

En el primer semestre de 2026, CARIAD aumentó sus ingresos en 250 millones de euros, hasta alcanzar los 815 millones de euros, impulsados por las entregas de software a los grupos de marcas. El resultado operativo mejoró significativamente hasta situarse en -855 millones de euros (año anterior: -1.172 millones de euros). Esta mejora pone de relieve el impacto del programa de transformación y la disciplina constante en materia de costes en todas las áreas.

Group Mobility

El resultado operativo se situó en 1.700 millones de euros (-7,6 %) debido al aumento de las provisiones para riesgos. Se observó una evolución positiva tanto en los nuevos contratos (+1,2 %) como en la cartera de contratos existente (+3,1 %).